Workers are losing sleep over their finances. According to a recent study of 1,200 U.S. workers by employee wellness solution FinFit and HR Dive’s studioID, 60% of workers felt worried and stressed when thinking about their financial situations in the past week. Nearly the same amount reported feeling anxious. And 46% said they had trouble sleeping due to their finances.

“This report underscores that the financially frustrated and the financially unhealthy are not just in the workforce. They are the workforce,” said Matt Bahl, vice president of workplace financial health at the nonprofit Financial Health Network. “Because of that, any organization that depends on people to do their work or to bring services and goods to the market needs to understand how financially frustrated or financially precarious their workforce is. Because it undoubtedly could have downstream impacts on their business.”

While it’s impossible to pinpoint a single source of widespread financial stress, the survey revealed several common struggles uniting respondents:

- Three in four respondents consider themselves to be living paycheck to paycheck.

- Seventy-two percent said they have no cash buffers or liquid savings, or these funds add up to less than $5,000.

- Eighty-three percent of respondents owe money on their credit cards every month, the median balance being $2,400.

The extensive financial hardships impacting workers should get employers’ attention, Bahl said. Employees do not experience financial stress in the confines of their personal lives. Unfortunately, it follows them to work — creating a challenge with both business and brand implications for employers.

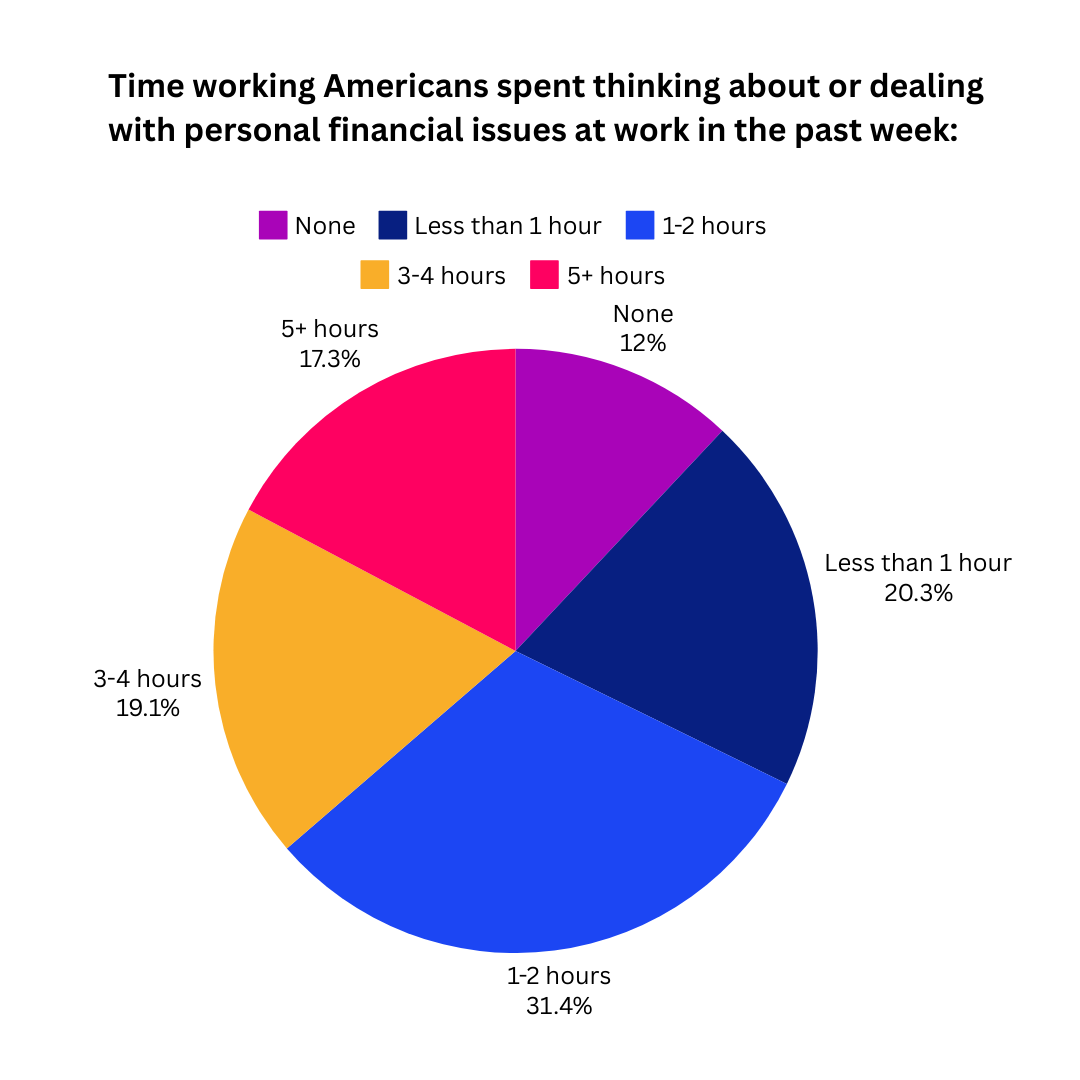

Risking productivity, quality and safety

More than a third of respondents (36%) said they spent three hours or more at work thinking about or dealing with personal financial issues, and 38% have taken days off of work to deal with these problems.

The impact of financial distractions is well documented. According to a report out of the University of Pittsburgh, a worker’s poor financial standing can hurt their performance outcomes. It can also limit their ability to take on new opportunities. The research specifically found that “financial worry decreases cognitive capacity, which subsequently hinders performance.” In its study of truck drivers, for example, those who were more worried about money proved to be more dangerous drivers.

Similar findings were published in Cornell University’s Industrial and Labor Relations Review. The report examined the impact of financial concerns on nursing aides. It found that aides’ money worries reduced their ability to attend to patient needs, which could potentially impact not only the quality of their care but also patient safety.

Bahl also noted that employers can build stronger brands when they identify and address employees’ struggles, including their financial ones.

“Most organizations claim to care about their workforce,” Bahl said. “So just from a brand alignment perspective, you would hope that organizations are doing things to solve the challenges their people are facing, as you would do for any key constituency that's driving your business forward.”

Employers can help — with the right tools

Employees don’t want to remain in a state of financial stress. They want to improve their finances — a goal employers may want to encourage, considering how financial frustration hurts performance. In FinFit’s survey, workers said they wanted to pay down debt, increase their savings and live more financially stable lives. These priorities were so important to them that they ranked them higher than making more money.

Alongside workers’ strong desire for financial improvement, the survey revealed systemic roadblocks keeping employees from making long-term progress. Workers, for instance, reported using credit cards to build up rewards, to improve or maintain their credit scores, to take advantage of stronger fraud and theft protections and to more easily track their spending.

But the vast majority of workers (83%) also said they’re left with large credit card balances each month. About half of respondents have a remaining balance between $500 and $3,000, and 36% are left with credit card debt totaling more than $3,000 — an increasingly weighty financial burden with the average credit card interest rate at an all-time high of 22.8%.

As workers struggle with credit card bills and more, it may come as little surprise that the most popular financial goals cited were paying down debt and building emergency savings. These desires translated to the benefits workers said they wanted from their employers: benefits designed to help them save money and pay down debt.

Most financial benefits fail to address these goals, however. Employer-provided tools typically come in the form of calculators, classes and coaches and focus on financial literacy. But workers said they wanted tools that would help them take action on their financial goals, save more money, pay down current debt and avoid future debt.

That’s why these tools are so popular among workers, Bahl said. “They solve a real material challenge. People face a 40- or 50-year history of wage stagnation and rising costs for healthcare, housing and childcare. You're not going to solve that through financial education [alone].”

When employers offer such tools, they help workers climb out of their current state of financial stress, improving their presence and focus at work. The survey indicated employers would see another return: Workers said they would be more likely to stay at their company, more likely to recommend it as an employer and more engaged in their work if they had these benefits.

“Inactivity by businesses is failure — and on a number of fronts,” Michael Woodhead, Chief Commercial Officer at FinFit said. “We have a responsibility to our employees to improve their financial wellness, which goes hand-in-hand with wellness. In addition to alleviating stress for workers, there’s also an enormous benefit to businesses, which thrive with happier, more loyal employees. I don’t see how we can continue to overlook the financial wellness needs of our workers.”

“Unsurprisingly, if you actually listen to your people and solve material challenges that they're facing, they're going to be more loyal to you,” Bahl said. “They're going to want to work harder for you.”

To improve performance and boost retention and engagement, employers need to provide benefits that target employees’ financial pain points and pave the way to progress. Get the latest research on these benefits and more in FinFit’s report: Inside the Wallets of Working Americans.